Berkshire 2000 Redux

2000, zero, zero, party over Oops, out of time So tonight I'm gonna party like it's 1999

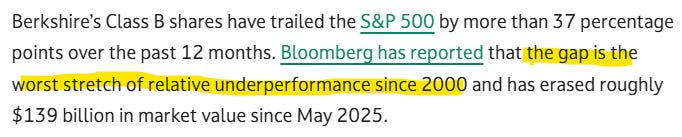

When Greg Abel took over as CEO of Berkshire Hathaway, my expectation was that the prevailing media narrative would be that Berkshire had lost it’s touch, was in decline, and was underperforming the S&P 500. That’s pretty much what happened almost immediately. There has been a flood of negative press about Abel and Berkshire recently. But one sentence in one of those articles stood out and gave me pause. It should have given the author pause too.

“The gap is the worst stretch of relative underperformance since 2000.” 2000 huh? You don’t say. Let’s go back to 2000 and see what was happening to Berkshire and the market around that time. Maybe we can learn some lessons from that period and apply them to the current situation for Berkshire and the market?

Party Like it’s 1999

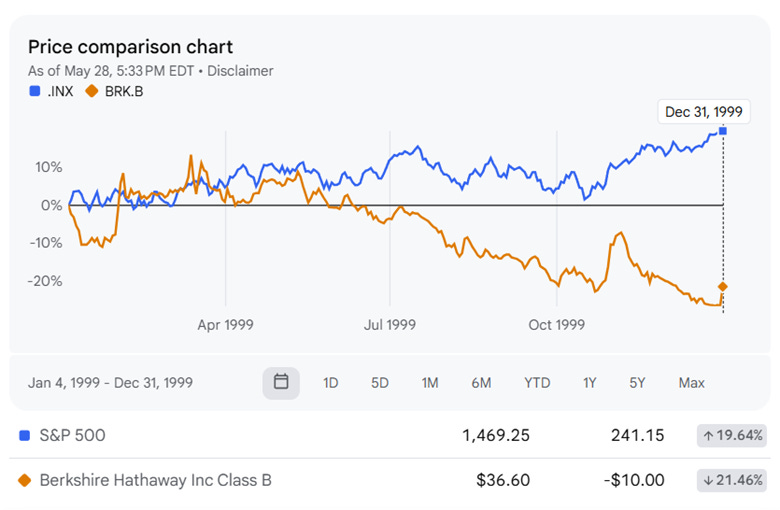

In 1999 Berkshire was experiencing one of its worst years of relative performance compared to the S&P 500 (to that point). The S&P 500 was marching steadily higher on the back of the “tech boom” (foreshadowing: soon to be reclassified as the tech bubble), while Berkshire saw it’s per share book value drop 0.5% and its stock price falling about 20%.

In his 1999 annual letter to shareholders, Buffett didn’t shy away from the poor performance and addressed it head on. “… we don’t own stocks of tech companies, even though we share the general view that our society will be transformed by their products and services. Our problem – which we can’t solve by studying up – is that we have no insights into which participants in the tech field possesses a truly durable competitive advantage. Our lack of tech insights, we should add, does not distress us…. If we have a strength, it is in recognizing when we are operating within our circle of competence and when we are approaching the perimeter. Predicting the long-term economics of companies that operate in fast changing industries is simply far beyond our perimeter… Fortunately, it’s almost certain that there will be opportunities from time to time for Berkshire to do well within the circle we have staked out… We have never attempted to forecast what the stock market is going to do in the next month or the next year, and we are not trying to do that now. But, equity investors currently seem wildly optimistic in their expectations about future returns.”

Skipping ahead a bit he continued “Berkshire will someday have opportunities to deploy major amounts of cash in equity markets – we are confident of that. But, as the song goes, “Who knows where or when?”

Included with the annual letter was an article Buffett wrote for Fortune Magazine. In it he argued that the market was setting itself up for disappointment, and while not predicting an immediate decline, he alluded to the market being overvalued.

Buffett noted that the hypothetical earnings yield (earnings/market value) on the Fortune 500 was 3.3% pre-tax[1] while the 10 year US Treasury Note yielded 1-2 percentage points higher than that. Basically, investors could earn a higher return on a “risk free” government security. Why would a rational investor own stocks? Because they thought stocks would continue to rise, just like they had done in the recent past.

He said there were three scenarios that could make the current prices rational:

(1) If interest rates fell

(2) If corporate profits increased

(3) You picked the obvious winners and “rode the wave”

Regarding the third point, he looked back at history to the automobile and airline industry explosions to see if riding the wave was a real possibility for the average investor.

Regarding automobiles “All told there appear to have been at least 2,000 car makers in an industry that had an incredible impact on people’s lives. If you had foreseen in the early days of cars how this industry would develop, you would have said, “Here is the road to riches.” So what did we progress to by the 1990’s? After corporate carnage that never let up, we came down to three US car companies… So here is an industry that had an enormous impact on America, and also an enormous impact – though not the anticipated one, on investors.”

Buffett’s conclusions on the Airline industry were just as dour “As of 1992, in fact – though the picture would have improved since then – the money that had been made since the dawn of aviation by all of this country’s airline companies was zero. Absolutely zero.”

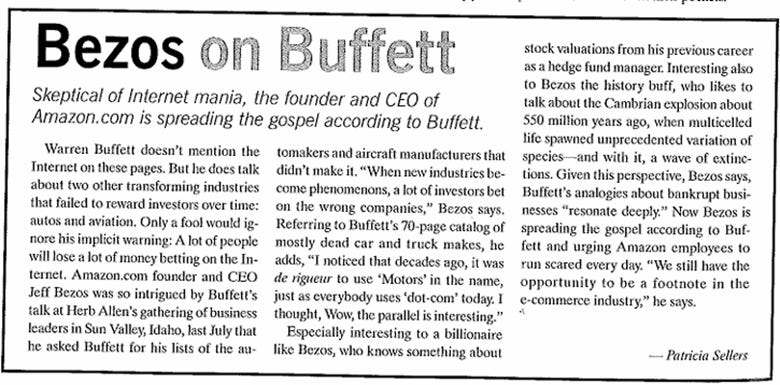

Buffett’s main points were that stocks were overvalued and that the odds of you picking a dot com winner were slim to none. As an aside, I’ll just include this blurb which was included in the article about a certain young entrepreneur named Jeff Bezos who read the article and urged his employees “to run scared” and that they still had “the opportunity to be a footnote in the ecommerce industry”. Wonder what ever happened to that guy and his “Amazon” company?

At the 1999 Berkshire Annual Meeting in Omaha, Buffett and Munger fielded some pretty hostile questions from the crowd. One in particular stands out and is worth watching:

“Now, with technology, computers, electronics, and software transforming our entire world and not just here around the world, I must admit that I personally invested in four technology computer software and aggressive growth mutual funds and made up all of my 1999 losses on Berkshire Hathaway. Are we asking too much as shareholders of Berkshire Hathaway for you men to put your brains to work and possibly speculate a little bit, maybe 10 percent of our money, into the only play in town, which seems to be technology, electronic? And I read your report, and I understand a lot of your reasoning that it’s difficult and it is difficult to project earnings of a lot and people are going to be a little bankrupt. Are they going to out of business? But isn’t there enough left in your brainpower to maybe pick a few and see what’s going on? Because I made over a hundred percent profit in 1999 on my aggressive position in the technology field, so that’s my question”

Buffett responded “The answer is we will never buy anything we don’t think we understand. And our definition of understanding is thinking that we have a reasonable probability of being able to assess where the business will be in 10 years…. There are all kinds of people that know how to make money in ways that we don’t. But, you know, it’s a free world and everybody can invest in those sorts of things. But they would be making a mistake, a big mistake, to do it through us. I mean, why pick a couple of guys like Charlie and me to do something like that when you can pick all kinds of other people that say they know how to do it….We had a lousy year in 1999, but the stock price did not calibrate with that in any perfect, or close to perfect, manner. And we’ve had good years other times, when the stock price is way overpriced or over-described what happened during the year. So we really measure all the time by the business. We think of it as a private business, basically, for which there’s a quotation. And if it’s handy to use that quotation, either in buying more stock or something of the sort, we may do it. But it does not govern our ideas of value….”

The 1999 Berkshire Annual Meeting took place on April 29, 2000, exactly one month and 19 days after the market peaked on March 10, 2000. The S&P 500 Went on to lose about 36% of its market value over the next 3 years.

And Berkshire? Well, over the next 3 years Berkshire and the S&P flipped with Berkshire massively overperforming, making up for all the underperformance in the 1999-2000 period and then some.

In the 2000 Letter to shareholders Buffett said: “The line separating investment and speculation, which is never bright and clear, becomes blurred still further when most market participants have recently enjoyed triumphs. Nothing sedates rationality like large doses of effortless money. After a heady experience of that kind, normally sensible people drift into behavior akin to that of Cinderella at the ball. They know that overstaying the festivities that is, continuing to speculate in companies that have gigantic valuations relative to the cash they are likely to generate in the future ¾ will eventually bring on pumpkins and mice. But they nevertheless hate to miss a single minute of what is one helluva party. Therefore, the giddy participants all plan to leave just seconds before midnight. There’s a problem, though: They are dancing in a room in which the clocks have no hands.

Last year, we commented on the exuberance - and, yes, it was irrational - that prevailed, noting that investor expectations had grown to be several multiples of probable returns…. Far more irrational still were the huge valuations that market participants were then putting on businesses almost certain to end up being of modest or no value. Yet investors, mesmerized by soaring stock prices and ignoring all else, piled into these enterprises. It was as if some virus, racing wildly among investment professionals as well as amateurs, induced hallucinations in which the values of stocks in certain sectors became decoupled from the values of the businesses that underlay them….

But a pin lies in wait for every bubble. And when the two eventually meet, a new wave of investors learns some very old lessons: First, many in Wall Street - a community in which quality control is not prized - will sell investors anything they will buy. Second, speculation is most dangerous when it looks easiest.

At Berkshire, we make no attempt to pick the few winners that will emerge from an ocean of unproven enterprises. We’re not smart enough to do that, and we know it….. We try, therefore, to keep our estimates conservative and to focus on industries where business surprises are unlikely to wreak havoc on owners. Even so, we make many mistakes: I’m the fellow, remember, who thought he understood the future economics of trading stamps, textiles, shoes and second-tier department stores.”

Applying the lessons of the 1999 – 2000 Period to Today

At Berkshire there has been a lot of change over the last few years. Charlie Munger passed away, Buffett has stepped down as CEO, Todd Combs (one of the two portfolio managers) has left, Ajit Jain (Berkshires head of Insurance) will likely retire in the next few years, and several other executives have left or are planning on leaving. The thing to understand about Berkshire, the thing that hasn’t changed, that likely will never change, is the extreme sense of rationality, the discipline, to maintain a long-term focus no matter what is going on around them. They are maintaining their discipline on the insurance underwriting side (unlike almost every other insurance company when they don’t feel that they are being appropriately compensated for risk they don’t write policies), on the equity investing side (they have been net sellers of stocks for years now), and on the acquisition side (have not had a major acquisition in years). Just because they are sitting on a pile of cash doesn’t mean it is burning a hole in their pocket. As Buffett said in the 1999 letter, they will have opportunities to deploy the cash, but no one knows when. If you are a Berkshire shareholder, you have to understand this, and come to terms with it.

As far as where we are in the market cycle. The market is consistently taking out new highs. There are a lot of head scratching market moves that seem to defy rationality (as I write this Dell is up 38% in premarket trading). The current PE for the S&P of 28 is very high. The subsequent ten year returns when the S&P’s PE is above 22 have all been negative (base rates matter). Many have compared todays market environment to the dot com bubble and 1999.

So is it 1999 now? Is it 2000? Valuations certainly seem disjointed from reality, and people definitely seem sedated by seemingly effortless returns. I really don’t know how this will play out and I don’t think anyone can answer these questions. What I do know is just like the ’99 –’00 period, Berkshire has stuck to its disciplined approach, is sitting on a mountain of dry powder (cash), and will be perfectly positioned to deploy large amounts of capital, should the opportunity present itself.

[1] Not including frictional costs of taxes and trading fees etc..

Trailing QQQ compounded returns as of last night’s close are:

10 years - 21.79% - 7.2x your initial investment

15 years - 19.58% - 14.6x your initial investment

These are exceptional returns. BRKB for reference is 12.8% over both time periods…..Still very good, yet “only” 3.3x and 6.1x.

It’s easy to understand why many salivate at the former and scoff at the latter. It’s human nature. I admit having been concerned about various market statistics for several years, which means I’ve underperformed. However, similar to some of the quotes you have from Buffett here, I just can’t jump on a bandwagon to chase performance of others.