Prosus - FY 2026 Update

The company achieved their revenue and aEBITDA targets, and the stock sold off anyway

Prosus FY 2026 Update

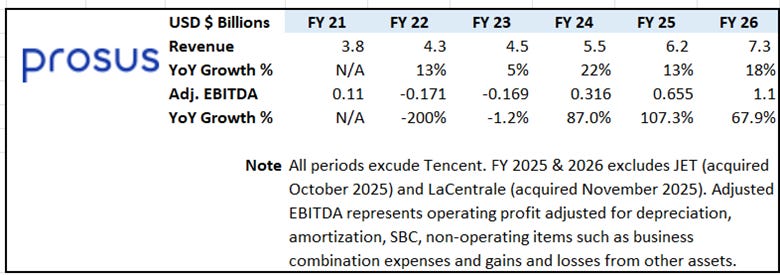

Prosus’s CEO (Fabricio Bloisi) released a letter this week providing some updates on how FY 2026 ended and how Prosus’s subsidiaries and investee companies were performing. We will have to wait till June for the full financial picture[1], but headline revenue and aEBITDA (excluding Tencent and some recent acquisitions) were very good. Revenue rose 18% to $7.3 billion and aEBITDA rose over 67% to $1.1 billion.

These are very promising numbers. My thesis on Prosus is very simple. Historically, Prosus’s investments (outside Tencent) have been money pits, sucking up capital and producing a steady stream of losses projected into the future with no end in sight. The market assigns these companies no value in Prosus’s market cap. I think this is wrong, and it’s borne out in the fundamentals. Prosus’s subsidiaries and investee companies have real value and are poised to grow (both their top and bottom lines). They will require continued investments, but these investments will produce near term results demonstrated in higher revenue and aEBITDA.

Separately, Tencent (which Prosus owns about 23% of) had a good 2025 as well. Revenue grew 10% to $107 billion and Net Income grew 13% to $32 billion. They put a lot of capex into AI investments, but Free Cash Flow still grew 17% to $28 billion. Despite having great fundamentals, Chinese technology stocks have been punished by the market for their significant spending on AI investments. I think this is similar to what happened to US tech at the end of Q4 2025. As long as Tencent’s fundamentals remain strong (which they should), the dislocation in the stock price should reverse. Prosus’s share of Tencent’s earnings for 2025 should be around $7.36 billion.

Some highlights from across Prosus’s ecosystem for 2025 include:

· iFood (food delivery - Prosus owns 100%) is transitioning from a food delivery app, to a quick commerce platform, expanding to new verticals like groceries and pharmaceuticals.

· iFood Pago (it’s fintech system) had triple digit revenue growth and “has reached scale”

· The meal voucher business (where employers can buy meals for their employees) serves 1 million users is growing 100% year over year

· Despegar (online travel – Prosus owns 100%) grew 30% in the Brazilian market. 17% of its revenues now come from iFood referrals, demonstrating the potential for synergies across their various platforms and ecosystems.

· OLX (online classifieds – Prosus owns 100%) growing revenues strongly and margins are expanding. OLX by itself had aEBITDA of over $450 million (about 41% of the $1.1 billion total for the period). It is utilizing AI to enhance the profitability of its platform and its usefulness to realtors and car dealers.

· Just Eat Takeaway (food delivery – Prosus owns 100%) JET will be a major test for Prosus. As a separate company JET never came close to being profitable and its revenues were erratic. Prosus closed on the JET acquisition in October 2025, and has made some quick progress in turning the company around. For FY 2027 they are expecting to do about $3.6 billion in revenue and $100 million in aEBITDA.

· PayU (payment aggregator – Prosus owns 100%) had $18 million of aEBITDA for FY 2026, up from -$25 million in FY 2025. PayU is serving as the payments provider for several Prosus investee companies in the Indian region including Rapido (ride hailing and logistics), Swiggy (food delivery), Ixigo (travel), Urban Company (home services), and Meesho (e-commerce).

iFood - Intense Competition

iFood is the #1 food delivery app in Brazil, but that position is constantly under threat. There have been several new entrants to the Brazilian market, like Meituan, which have deep pockets, and are spending aggressively to try and unseat iFood. Bloisi (Prosus’s CEO) notes that the competition will spend about $1.5 billion in FY 2027. He believes this level of spend is unsustainable, but iFood will step up its investments, to maintain and even expand its position. As a result of this increased spending, he estimates FY 2027 aEBITDA will be reduced by $100-150 million.

Most news agencies ignored all the other positives that were in the CEO letter and honed in on the FY 2027 aEBITDA information. As a result, (I believe) the stock dropped about 7.2% on European exchanges the day the letter was released.

Capital Allocation

Prosus is repurchasing shares at about a $5 billion annual rate. This is especially value accretive to shareholders (that don’t sell), because the stock is so underpriced relative to its intrinsic value. They have repurchased over $50 billion dollars worth of shares in the last 4 years.

Prosus has signaled that they will not make any large acquisitions in FY 2027[2]. In 2026 they sold off over $2 billion of non-strategic[3] asset sales. This will continue into FY 2027.

Prosus - Stock Performance

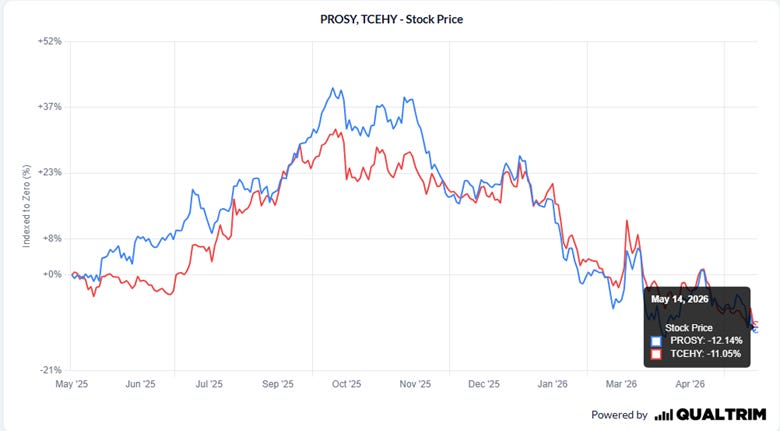

Over the past year, Prosus’s stock performance hasn’t been great. The stock has declined by 12% pretty much in line with Tencent, which declined by 11%. This indicates that Prosus’s performance, as a stock, is still levered to Tencent. My thesis is that as Prosus’s businesses (excluding Tencent) generate more revenue and earnings, the relationship between Prosus and Tencent will start to decouple, and their performance will be less correlated. As Tencent accounted for over 90% of Prosus’s core headline earnings (Net income: $12.37 billion / Tencent earnings: $5.7 billion / Tencent share sales: $6 billion), this will take a long time (years) to play out. Patience is necessary here.

Net Asset Value Calculation

Prosus’s Net Asset Value (NAV) is estimated to be $157.3 billion (down from $204 billion in 02/26). Based on the current market cap of around $100 billion, the NAV discount is now around 64% (up from 43% in 02/26).

Conclusion

With the stock trading back at a single digit price to earnings (7.85x) I think there are three likely scenarios here:

· Best case scenario – Prosus’s subsidiary companies perform very well and continue to grow rapidly in revenue and aEBITDA. Prosus succeeds in integrating its companies into superapps delivering a variety of products and services on unified platforms. Tencent continues to do well also. As a result Prosus stock receives a higher multiple in the midteens and the increased earnings lead to a significantly higher share price.

· Mid case scenario – Prosus’s subsidiary companies perform well (growing revenue and aEBITDA) but the superapp integration is unsuccessful. The companies remain standalone businesses and platforms, and don’t realize the expected synergies. Tencent continues to do well. The increase earnings lead to a slightly higher share price, but the earnings multiple does not rerate and remains low.

· Worst case scenario – There is some sort of geopolitical event and Tencent’s value is severely impaired, leading to a corresponding drop in Prosus’s share price.

I think this is an opportune time to buy Prosus, but it does come with considerable risks. To make this investment you have to be patient and comfortable watching paint dry. This is a play that will take years to work itself out

Disclaimer: The information provided on Lots of Value is for general informational and educational purposes only. It is not intended to be, and should not be construed as, professional financial, investment, tax, or legal advice. Lots of Value is not a registered investment advisor or fiduciary.

The author(s) or owner(s) of this blog may currently hold positions, or plan to initiate positions, in the securities, ETFs, or other financial instruments discussed in these posts. We disclose this to maintain full transparency with our readers. However, our ownership status may change at any time without notice, and we are under no obligation to update this blog to reflect when a position has been sold or adjusted. You should not assume that our interests are aligned with yours; always perform your own due diligence before making any investment.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Any decision to invest should be made only after consulting with a qualified professional and performing your own due diligence. Lots of Value makes no representations as to the accuracy, completeness, or suitability of the information provided and will not be liable for any losses, injuries, or damages from the display or use of this information.

[1] Prosus is based in Europe and releases financial statements twice a year.

[2] But if the right opportunity presented itself, I’m sure they would change their minds.

[3] Non-strategic here means minority interest investments in companies (this excludes the sale of Tencent shares)